Annual monitoring

It's about public confidence

We are required to monitor, encourage and facilitate charities' compliance with charity law and to increase public confidence in charities. It is a legal requirement for all charities to send a copy of their accounts to OSCR.

This page sets outs the annual monitoring cycle and what happens if information is not provided on time.

What information do you need to send?

Every year you must send us your:

All the information is needed to complete the annual monitoring requirements.

Using our Online Services makes the process easier and helps you to get it right.

The information collected from the online annual return helps OSCR maintain an accurate and useful Scottish Charity Register and allows us to monitor and regulate charities operating in Scotland.

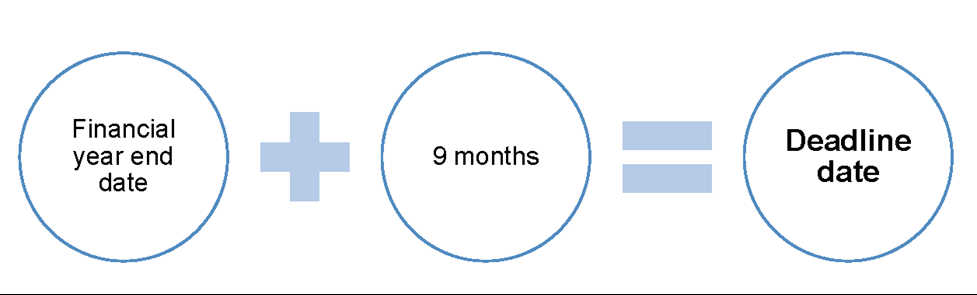

When do you need to send the information?

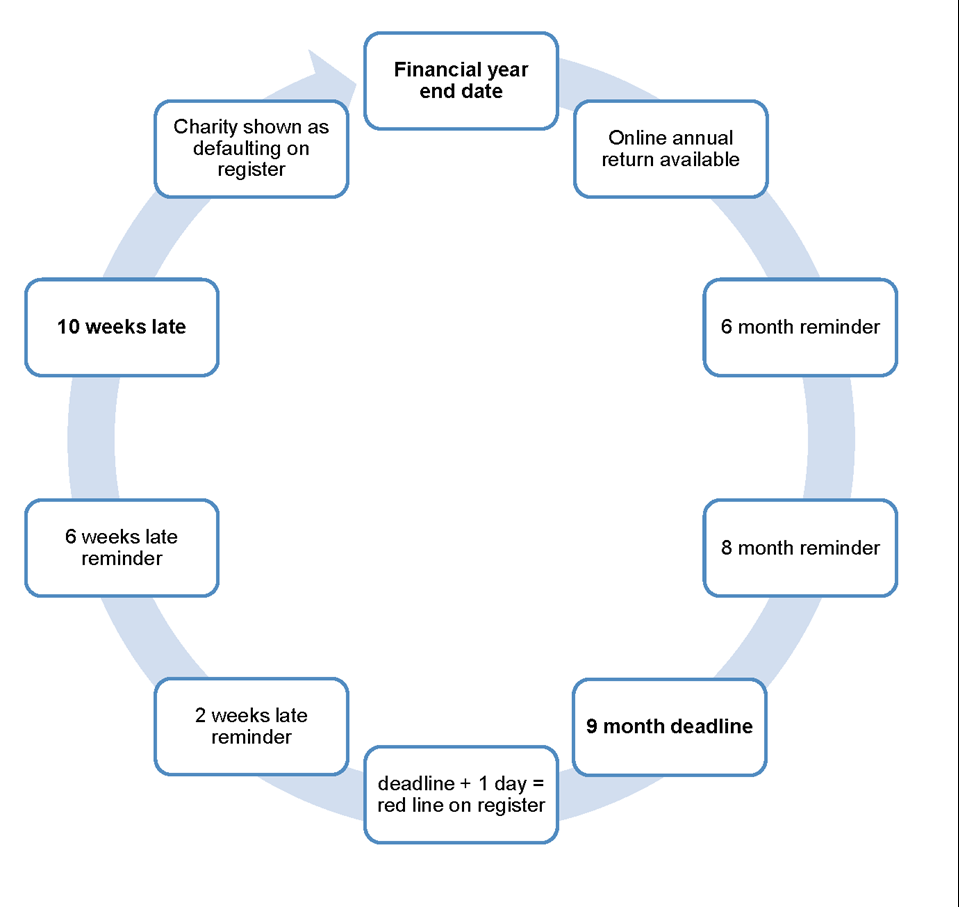

You have 9 months from your financial year end date to send the information:

Why you need to send the information

All charities registered in Scotland have a legal duty to provide OSCR with annual reports and accounts every year. This is one of the charity trustee duties in terms of The Charities and Trustee Investment (Scotland) Act 2005.

Without the information there's no evidence to show OSCR and others that you are carrying out activities and providing public benefit.

What does OSCR do with the information?

- We do a basic check of all the information to make sure there are no obvious mistakes.

- We don’t do a full check of every set of reports and accounts.

- We do detailed checks throughout the year of some charities reports and accounts.

- Where we identify issues we will follow up directly with the charity.

- Where we identify common trends we will highlight these and provide guidance where necessary.

- We publish the reports and accounts of all charities with an income of £25,000 or more and all SCIOs on the Scottish Charity Register.

We are cross-border charity registered in England and Wales, what do we need to do?

There are around 1020 charities that are registered both with us and with the Charity Commission for England and Wales, known as cross-border charities.

If you are a cross-border charity you must complete Section A of the online Annual Return and one additional question about your activities in Scotland.

In England and Wales the deadline for submitting accounts is 10 months after the financial year end date. However, cross-border charities must still submit to OSCR within 9 months of their financial year end date, which is the same as the timescales under company law.

See our guidance for cross-border charities for more information.

What happens if the information is not sent?

Once the deadline date has passed you are late in providing the information. A red line and the number of days your charity is late by will appear on your Scottish Charity Register entry to highlight this to the public and others, such as funders.

This red line will come off when your return is up to date. However, your annual return submission history will continue to show late returns for five years.

Our aim is to achieve compliance, so we will send you reminder emails until 10 weeks after your deadline date. After this point the charity is classed as defaulting.

What if the information is not sent within 10 weeks of the deadline date?

If your information is not sent to us within 10 weeks of the deadline date the charity will be shown as defaulting on the Scottish Charity Register. This means the charity has defaulted on the legal requirement to provide OSCR with annual reports and accounts, which is a breach of the charity trustees’ duties. This is misconduct and we have powers take action against charity trustees where appropriate and proportionate.

Without this information there's no evidence to show OSCR and others that you are carrying out activities and providing public benefit. This means there is no evidence that your charity is meeting the charity test and ultimately charity status can be removed.

In general, if a charity does nothing for a prolonged period, it is unlikely to be providing public benefit, and this may result in it failing the charity test. There are some exceptions where this principle does not apply. We call these ‘inactive charities’.

One type of inactive charity is where a charity is set up to act if a particular event occurs in the future, and where public benefit is provided because the charity is there ‘just in case’.

For example:

- a charity is set up to relieve the needs of those who might be made homeless by flooding in a flood-prone area of Scotland – there may be no floods and therefore no activity for several years, but the existence of the charity allows prompt relief should a flood occur.

Another type of inactive charity is a ‘legacy’ charity:

- where one charity is replaced or taken over by another, the charity which has been taken over continues purely to receive legacies and pass them to the new charity – there may be long periods where no money is received or transferred, but the ‘legacy’ charity provides benefit by making sure that donations reach the right destination.

Where an inactive charity remains on the Register, it will still need to meet all the requirements of being a charity.

In particular it must:

- meet the charity test

- have charity trustees who comply with all the charity trustee duties

- comply with annual monitoring: preparing and submitting accounts, trustees’ annual report and the Online annual return.

If your charity is removed from the Register, you must still prepare and submit accounts to us for any outstanding charity assets held at the time of removal. Read our Former Charities page for more information.