2. Preparing accounts

2.1 The types of accounts that can be prepared

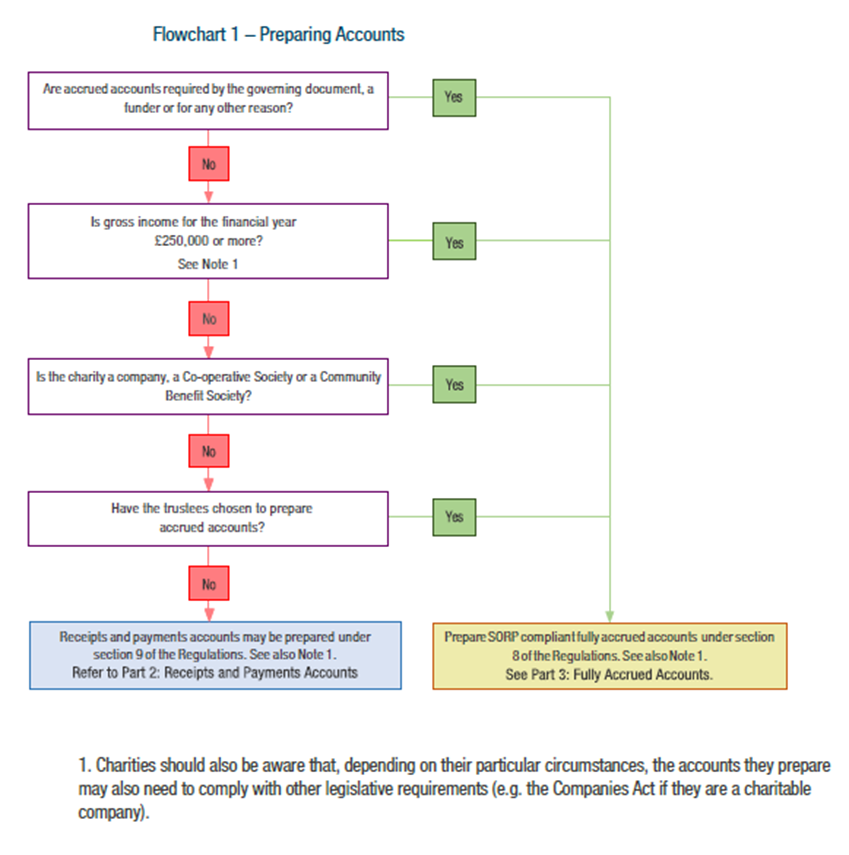

Charities must prepare accounts in one of two ways depending on several factors. These are briefly:

- receipts and payments

Receipts and payments accounts are a simple form of accounting that consist of a summary of all monies received and paid by the charity during its financial year in both cash and via the bank account, along with a statement of balances at the year end.

- fully accrued

Fully accrued accounts record all the transactions of the charity in the financial year. Fully accrued accounts include income which a charity is due to receive and expenses which are due to be met.

Fully accrued accounts must be prepared in accordance with the methods and principles of the Accounting and Reporting by Charities: Statement of Recommended Practice (the SORP).

2.2 Which type of accounts should we prepare?

Normally a charity’s gross income for a given financial year will determine the type of accounts to be prepared for that particular year. However, if:

- the charity’s governing document says it should prepare fully accrued accounts, or

- the charity trustees have taken a decision to prepare fully accrued accounts,

- any third party requirements, for example funders, or

- any enactment says that the organisation should prepare fully accrued accounts (for example, the provisions of the Companies Act 2006 mean that charitable companies must prepare fully accrued accounts)

then fully accrued accounts must be prepared even if the charity’s gross income would otherwise allow accounts to be produced on the receipts and payments basis.

Fully accrued accounts must follow the SORP and, if independently examined, be examined by a qualified independent examiner. Charity trustees should fully consider the implications of deciding to prepare fully accrued accounts if they are not otherwise required.

Apart from the statutory requirement, any requirement of the governing document or third party reference to accounts providing a true and fair view of the financial affairs of the charity would require the preparation of fully accrued accounts.

See the flowchart below called ‘Preparing Accounts’ to determine the type of accounts that must be prepared.

Once the charity has established the type of accounts required for the financial period they can read our receipts and payments accounts guidance and fully accrued accounts guidance for more detailed information on the requirements specific to the type of accounts being prepared.