Social Enterprise FAQs

This guidance outlines the position under Scottish charity law for Social Enterprises thinking about becoming a charity and is based on our experience of applications from organisations who class themselves as Social Enterprises. It is also relevant for existing charities thinking of setting up a Social Enterprise trading arm.

| As the Scottish Charity Regulator we are not primarily concerned with whether an organisation calls itself a Social Enterprise or not. What we focus on is whether it is a charity or can become a charity. |

Download the PDF version

1. What is a Social Enterprise?

2. How do Social Enterprises work?

3. Can a Social Enterprise be a charity in Scotland?

4. How does OSCR decide if a Social Enterprise can be a charity?

5. What are the common challenges for Social Enterprises becoming a charity?

6. What does OSCR need to know?

7. Is being a charity right for you?

8. Where can I get more help and advice?

1. What is a Social Enterprise?

There is no legal definition of a Social Enterprise in Scotland, and different stakeholders have their own views about what the characteristics of a social enterprise are. However, there are a number of descriptions, which share common concepts:

- Social Enterprise in Scotland Census 2015: Businesses that trade for the common good rather than the unlimited private gain of a few. They tackle social problems, strengthen communities, improve people’s life chances and protect the environment. They reinvest any profits to deliver on this social purpose.

- Scottish Government: Businesses with primary social objectives whose surpluses are principally reinvested for that purpose in the business or in the community, rather than being driven by the need to maximise profit for shareholders and owners.

- Social Enterprise Scotland: A dynamic and inspiring way of doing business. Social enterprises are innovative, independent businesses that exist specifically for social and/or environmental purposes.

- Voluntary Code of Practice for Social Enterprise in Scotland: The code sets out five essential elements of a social enterprise.

It’s generally recognised that a Social Enterprise is a business and operates on a profit-making basis, putting those profits back into the social mission or purpose of the organisation.

The term ‘Social Enterprise’ describes the nature of a business, not its legal form. Social Enterprises can take different legal forms, as can charities.

Back to the top

2. How do Social Enterprises work?

Social Enterprises try to be financially independent through trading, by selling goods and/or services for a profit. This profit is ploughed back into the Social Enterprise and its mission. This self generated income gives Social Enterprises greater flexibility about how to apply their assets.

Some charities carry out trading, but not all of them do. Many charities have ‘non-trading’ income streams, such as donations or grant funding.

In general, there are two types of Social Enterprise trading:

- Trading activity that links directly to the social/environmental mission of the Social Enterprise (known as ‘primary purpose’ trading in tax law).

| For example: A cafe that has been set up primarily to provide training and work experience for people with learning difficulties. The majority of those working in the cafe are beneficiaries and other employees are limited to those needed to ensure adequate support and training. Any profits made from the trading are put back into running the cafe. This could further charitable purposes of advancing education or relieving the needs of those disadvantaged by disability. |

2. Trading activity undertaken to generate income that is applied to the social/environmental mission of the Social Enterprise (known as ‘non-primary purpose’ trading in tax law).

| For example: A cafe run purely to make a profit for a social enterprise to cover the costs of another activity that advances its social mission (such as providing free education classes). |

Back to the top

3. Can a Social Enterprise be a charity in Scotland?

Yes, if it can pass the charity test. The Social Enterprise in Scotland Census 2015 found that there are around 3,500 Social Enterprises registered as charities in Scotland.

The Charity Test

The charity test is set out in the Charities and Trustee Investment (Scotland) Act 2005 (the 2005 Act). To pass the charity test an organisation:

- must have only charitable purposes and

- its activities must provide public benefit in Scotland or elsewhere.

When we look at whether or not an organisation provides public benefit, we need to consider if:

- there is any private benefit from the organisation’s activities

- there is any disbenefit to the public from its activities

- there is any unduly restrictive conditions on accessing the benefit the organisation provides.

Not everything that is ‘beneficial’ in a general sense is necessarily public benefit in terms of the charity test. An activity can only provide public benefit if it is advancing a charitable purpose.

| For example: It may be ‘beneficial’ for a village community to have a grocery or convenience store, but this does not automatically make it charitable to provide one if the shop is run on a commercial basis for private benefit. |

To pass the charity test any private benefit must be incidental to the organisation’s activities that advance its purposes:

- incidental means that the private benefit is a necessary result or by-product of the organisation’s activities and is not an end in itself.

In addition, an organisation will fail the charity test if:

- its governing document allows its assets to be distributed or applied for non-charitable purposes

- its governing document expressly permits government Ministers to direct or control its activities

- it is a political party or one of its purposes is to advance a political party.

Back to the top

4. How does OSCR decide if a Social Enterprise can be a charity?

We apply the charity test to Social Enterprises in the same way as any other organisation wishing to become a charity.

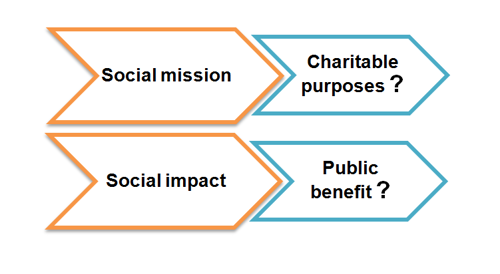

All Social Enterprises have a social mission: a primary objective to achieve social and/or environmental benefit, and aim to achieve a social impact. However, there is no guarantee that the social mission will consist of exclusively charitable purposes.

We look to see if the purposes in the governing document are entirely charitable and consistent with one or more of the charitable purposes set out in the 2005 Act.

If the organisation has only charitable purposes then we look at whether its social impact provides (or intends to provide) public benefit.

Sometimes the connection between the social mission and charitable purposes, and the social impact and public benefit is obvious, sometimes it is not. If it’s not, then we will need to ask more questions about the Social Enterprise - see question 6 for more detail.

An organisation will fail the charity test if its governing document allows it to use any of its assets for a purpose that is not a charitable purpose under the 2005 Act. This applies during the lifetime of the organisation and when the organisation is being wound up.

A charity’s governing document must not allow profits from trading to be paid to members, shareholders or other individuals as dividends or bonuses.

How we make our decision:

We look at the organisation’s governing document, the whole picture of what the organisation does (or plans to do), and the benefit the activities provide. We also look at any private benefit, disbenefit or undue restriction.

For more information see: Meeting the Charity Test Guidance.

| OSCR regulates Social Enterprise charities in the same way as any other charity. |

Back to the top

5. What are the common challenges for Social Enterprises becoming a charity?

Below are some of the most common challenges we see Social Enterprise’s face when trying to meet the charity test:

We have to compare any public benefit provided (or intended) against any private benefit there may be.

If it appears to us that a Social Enterprise has been set up wholly or mostly for the private benefit of an individual or group of people, it will not pass the charity test.

We see applications to become a charity from organisations describing themselves as Social Enterprises where the starting point appears to be an attempt to make an existing business profitable. The tax and rates advantages enjoyed by charities may be a motivator for a business to attempt to reduce its overheads.

We also see applications where the payment or business interests of an individual are central to the proposal. This is of concern especially where we find that the person setting up the Social Enterprise decides to employ themselves as the Chief Executive before we receive an application to become a charity.

These are both examples of possible private benefit. To pass the charity test any private benefit must be incidental to the organisation’s activities that advance its purposes:

- incidental means that the private benefit is a necessary result or by-product of the organisation’s activities and is not an end in itself.

If registered as a charity there are further implications if a charity trustee or a person connected to them is going to be paid. See our guidance on Charity Trustee remuneration for more information.

- Training and employment

Primary purpose trading (links directly to the social/environmental mission)

A common example of primary purpose trading that can be charitable is providing training and work experience in order to create opportunities for those who face significant barriers to employment.

For example:

- people with chronic physical or mental health problems

- people with learning difficulties

- women returning after career breaks to bring up children

- people with caring responsibilities who need to work flexibly

- ex-offenders

- people of low educational attainment

- people recovering from alcohol or substance misuse.

In these cases we look to see that:

- participants are employed for a limited period of time

- on-the-job training is complemented by other types of training (for example work skills or life skills) or the opportunity to gain vocational qualifications

- support or advice is provided to address other barriers to work, like homelessness or substance abuse

- the majority of workers in the business are from the target beneficiary group.

Many Social Enterprises identify the creation of new jobs as evidence of their social impact but this does not necessarily mean they are advancing a charitable purpose and providing public benefit. Simply employing people in order to carry on a trade does not relieve unemployment in a charitable sense unless it can be demonstrated that the jobs will be for those who are genuinely disadvantaged in the labour market, for example adults with learning difficulties.

- Delay in providing public benefit

Social Enterprises, like any business, may take some time to become profitable and are subject to the risks and uncertainties of the market for their goods and services.

In cases like this we often need to see a business plan or projections, which demonstrate when, profit is likely to start and therefore when public benefit is likely to be provided to achieve the organisation’s charitable purposes.

|

For example: The public benefit would not come from the café itself but from the grants made to other projects. If the café generates little or no profit then it will be difficult to see how public benefit is provided. |

Back to the top

6. What does OSCR need to know?

When we look at applications to become a charity from Social Enterprises we need to ask the following questions:

- Can we identify the applicant’s social mission?

- Can we link the social mission entirely to charitable purposes?

- Is there a sufficient asset lock?

- Will the trading activity directly advance the charitable purpose(s) (primary purpose trading)?

- If not (the trade is to raise funds), will the trade be carried out directly by the applicant or through a subsidiary?

- Will there be a delay in providing public benefit?

- Will there be any private benefit to the proposed charity trustees or others?

Where the answers to these questions are unclear, we will need the applicant to provide us with more information. If you are unable to answer all or most of these questions then you should get some advice before applying to become a charity. See question 8 for sources of help and advice.

Back to the top

7. Is being a charity right for your Social Enterprise?

There are advantages in becoming a charity, but you will need to consider whether this is the best option for your Social Enterprise. Registration as a charity tells the public that:

- your organisation meets the charity test

- your organisation is regulated by the Scottish Charity Regulator

- the charity trustees (the people who control and manage it) must act in certain ways and provide certain information to us and to the public.

Being a charity can give you access to different opportunities and tax reliefs; however, it can also restrict the type of activities an organisation carries out. See our Becoming a Charity in Scotland page for more details.

There are alternatives to being a charity that may suit your Social Enterprise better. For example a Community Interest Company or a Community Benefit Society.

Back to the top

8. Where can I get more help and advice?

- Third Sector Interface (TSI)

- Social Enterprise Scotland

- Senscot

- Firstport

- Social Enterprise Academy

- Community Enterprise

- Highlands and Islands Enterprise

- Social Investment Scotland

- Social Firms Scotland

- CEIS (Community Enterprise in Scotland)