Trustee Remuneration

Information on charity trustee remuneration and the conditions for remuneration.

The 2005 Act states that remuneration of charity trustees may be any direct or indirect payment or benefit, including a benefit in kind. It can be for:

- being a charity trustee

- a contract of employment

- for other services to or on behalf of the charity.

Charity trustees must act in the interest of their charity and any personal benefit, whether direct or indirect, must be treated with caution. Section 67 of the 2005 Act states that a charity trustee must not be remunerated from charity assets unless certain conditions are met.

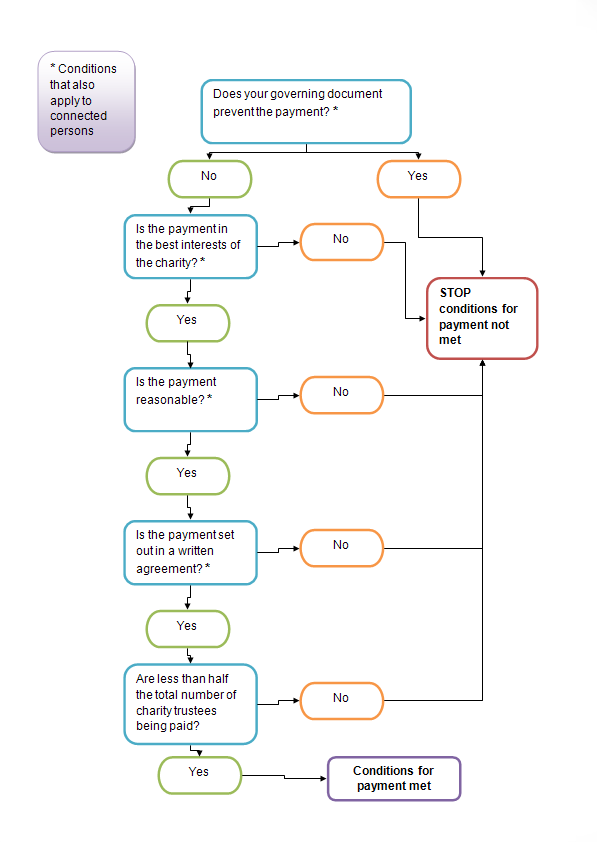

Conditions for remuneration

The conditions which allow remuneration are:

- the maximum amount of the remuneration is set out in a written agreement

- the maximum amount of the remuneration is reasonable in the circumstances

- the charity trustees are satisfied, before entering the agreement, that it is in the interest of the charity for that person to provide those services for that amount

- immediately after entering into the agreement, less than half of the total number of charity trustees are directly or indirectly remunerated

- the charity's governing document does not prohibit the remuneration of charity trustees.

There are some exceptions to meeting the above remuneration conditions. Further information on these exceptions is available from our Guidance and Good Practice for Charity Trustees.